Montana Ranger

Well-Known Member

- First Name

- John

- Joined

- Oct 19, 2019

- Threads

- 2

- Messages

- 303

- Reaction score

- 913

- Location

- Missoula, MT

- Vehicle(s)

- 2019 Ranger Lariat

- Thread starter

- #1

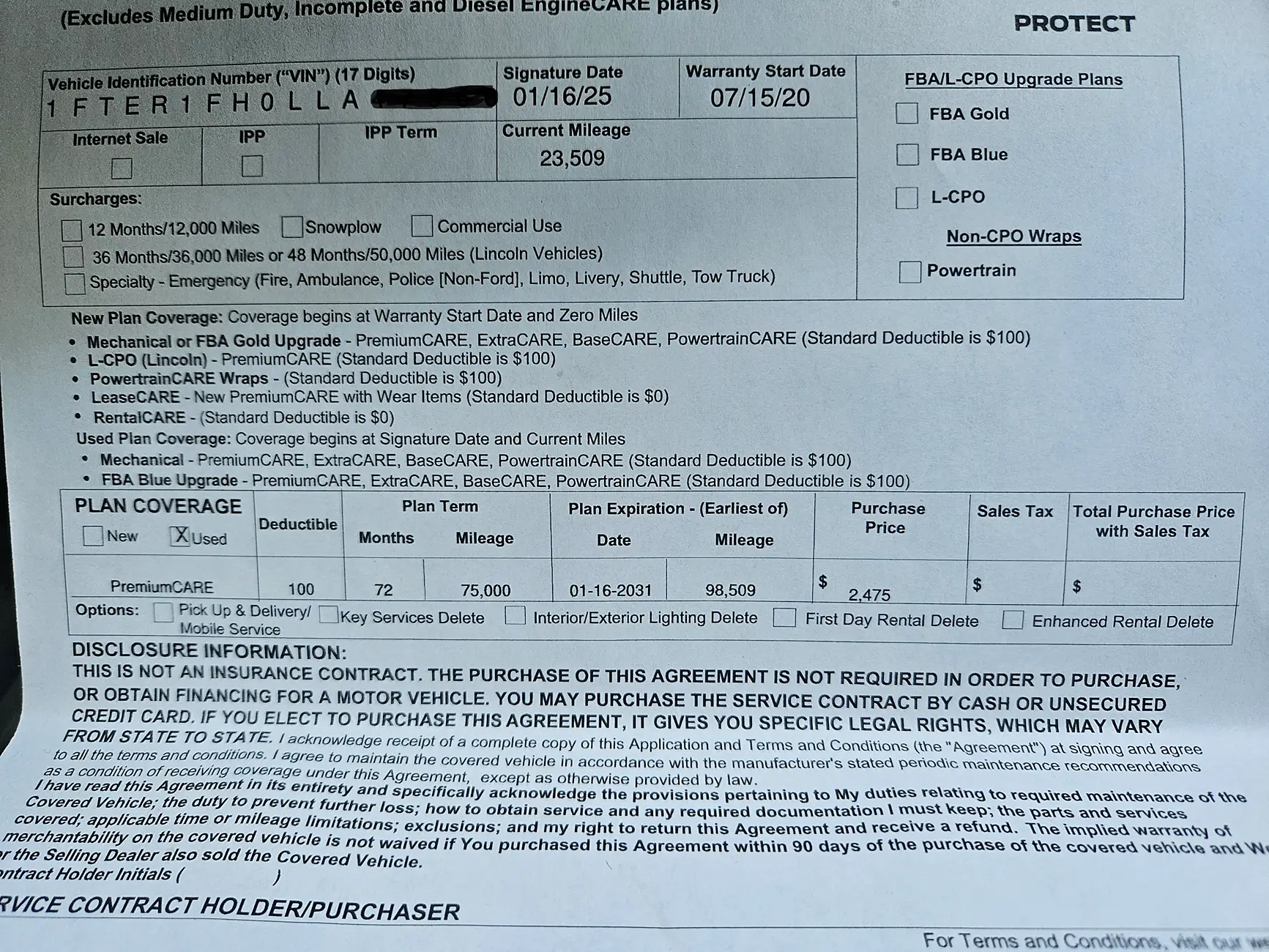

I have a 2019 Ranger SuperCab Lariat with close to 67,000 miles and have never had any noteworthy mechanical issues. (I'm still on the original battery!) The 7-year/100,000 mile extended warranty I purchased will be up this fall, and Ford is now offering to extend it for another 36 months for a total of $5,004.

It's always been my plan to keep this truck to around 120,000 miles, so I'm a little over half-way there. I typically expect to get 250,000 out of most of the vehicles I've owned, but half of the miles on my Ranger have been towing, which is a lot of hard work on the small 2.3 twin-turbo, especially in the higher altitude mountainous environment we're mostly in. And that combined with this engine's complexity makes me question the long term reliability of it and the 1080R beyond 120,000. I'm budgeted to replace my Ranger in a few years, so if it starts to show signs of impending expensive repairs, I'm am prepared to move on.

So I've decided to hold on to my $5,004 that will either deal with any kinda-major issue that pops up in the next few years or will go towards the new truck when it's time.

But for kicks-n-giggles, I thought I'd throw the question at ChatCPT to see what it said. Here's my question and its response:

Would like to do some calculus regarding the economics of extending a warranty on our truck. 2019 Ford Ranger Lariat. Good condition. No mechanical issues. 68577 miles. Half of the miles are from towing our camper spring through fall, which puts a lot of stress on its complex small twin turbo engine. So over the long run I have no expectation that this truck will last 250,000 miles like most of my vehicles have. My current expectation is to keep thjs truck until around 120,000 miles at which point we have budgeted to replace it in 4 or 5 years. I am currently being offered a relatively comprehensive extended warranty for 36 months for a total of $5004 with a $500 deductible. At this point, I think that if before 120,000 miles something serious were to fail, it would be better at that point to either fix out of pocket, or devote the $5004 dollars to a new truck. What is your analysis of this situation?

-

John, I think your intuition is probably correct, and I'd analyze it as a capital allocation problem, not a mechanical problem.

Let's look at the numbers.

Option A: Buy the warranty

Option B: Self-insure

Put the $5,004 in the "future truck fund."

You already have:

What would have to happen for the warranty to pay off?

Remember:

You pay $5,004 regardless.

With a $500 deductible, the warranty only starts to beat self-insurance if you incur significantly more than $5,500 of covered repairs.

Examples:

Repair bill = $2,000

Warranty:

Repair bill = $4,000

Warranty:

Repair bill = $6,000

Warranty:

Repair bill = $10,000

Warranty:

What are the likely failures?

On a 2019 Ranger 2.3 EcoBoost:

Expensive items include:

The question isn't:

"Could a $7,000 repair happen?"

It could.

The question is:

"What is the probability of a $7,000+ covered repair before 120,000 miles?"

My personal estimate is:

The towing factor

I agree with you that towing changes the analysis.

Your truck has not lived an easy life.

However:

The opportunity cost

This is the biggest factor for me.

If you invest the $5,004 in the replacement vehicle fund:

At a modest 5% return:

Another way to think about it

Suppose the worst happens.

At 105,000 miles:

Your truck is still worth something.

You still planned to replace it around 120,000 anyway.

The repair doesn't necessarily destroy your overall economics.

My conclusion

If you were planning to:

But given:

I would put the $5,004 into the replacement truck fund and self-insure.

The warranty company is betting that your covered repairs over the next 36 months will cost them less than $5,004 plus deductible income. Historically, that's usually a good bet for them.

For someone in your financial position and with a defined exit plan for the truck, I think self-insurance is the higher expected-value decision.

It's always been my plan to keep this truck to around 120,000 miles, so I'm a little over half-way there. I typically expect to get 250,000 out of most of the vehicles I've owned, but half of the miles on my Ranger have been towing, which is a lot of hard work on the small 2.3 twin-turbo, especially in the higher altitude mountainous environment we're mostly in. And that combined with this engine's complexity makes me question the long term reliability of it and the 1080R beyond 120,000. I'm budgeted to replace my Ranger in a few years, so if it starts to show signs of impending expensive repairs, I'm am prepared to move on.

So I've decided to hold on to my $5,004 that will either deal with any kinda-major issue that pops up in the next few years or will go towards the new truck when it's time.

But for kicks-n-giggles, I thought I'd throw the question at ChatCPT to see what it said. Here's my question and its response:

Would like to do some calculus regarding the economics of extending a warranty on our truck. 2019 Ford Ranger Lariat. Good condition. No mechanical issues. 68577 miles. Half of the miles are from towing our camper spring through fall, which puts a lot of stress on its complex small twin turbo engine. So over the long run I have no expectation that this truck will last 250,000 miles like most of my vehicles have. My current expectation is to keep thjs truck until around 120,000 miles at which point we have budgeted to replace it in 4 or 5 years. I am currently being offered a relatively comprehensive extended warranty for 36 months for a total of $5004 with a $500 deductible. At this point, I think that if before 120,000 miles something serious were to fail, it would be better at that point to either fix out of pocket, or devote the $5004 dollars to a new truck. What is your analysis of this situation?

-

John, I think your intuition is probably correct, and I'd analyze it as a capital allocation problem, not a mechanical problem.

Let's look at the numbers.

Option A: Buy the warranty

- Cost: $5,004

- Deductible: $500 per claim

- Coverage: 36 months

- Current mileage: 68,577

- Expected ownership: to about 120,000 miles

- Miles remaining: about 51,000 miles

Put the $5,004 in the "future truck fund."

You already have:

- a replacement plan

- a replacement budget

- no current mechanical issues

Remember:

You pay $5,004 regardless.

With a $500 deductible, the warranty only starts to beat self-insurance if you incur significantly more than $5,500 of covered repairs.

Examples:

Repair bill = $2,000

Warranty:

- You pay $5,004 + $500 deductible = $5,504

- You pay $2,000

Warranty:

- $5,504

- $4,000

Warranty:

- $5,504

- $6,000

Warranty:

- $5,504

- $10,000

On a 2019 Ranger 2.3 EcoBoost:

Expensive items include:

- turbocharger

- transmission

- transfer case (if 4WD)

- HVAC

- electronics

- infotainment

- power modules

The question isn't:

"Could a $7,000 repair happen?"

It could.

The question is:

"What is the probability of a $7,000+ covered repair before 120,000 miles?"

My personal estimate is:

- possible

- but not high enough to justify a $5,004 premium

I agree with you that towing changes the analysis.

Your truck has not lived an easy life.

However:

- Half the mileage towing a camper is not commercial abuse.

- Most drivetrain damage from towing would often start showing symptoms before 120,000 miles.

- You're already at nearly 70,000 miles without issues.

This is the biggest factor for me.

If you invest the $5,004 in the replacement vehicle fund:

At a modest 5% return:

- 4 years ≈ $6,100

- 5 years ≈ $6,400

Suppose the worst happens.

At 105,000 miles:

- Turbo fails

- Repair cost = $3,500

Your truck is still worth something.

You still planned to replace it around 120,000 anyway.

The repair doesn't necessarily destroy your overall economics.

If you were planning to:

- keep the truck to 200,000+ miles

- rely on it for income

- or could not absorb a major repair

But given:

- current mileage 68,577

- no issues

- replacement already budgeted at ~120,000 miles

- ability to absorb repairs

- $5,004 upfront cost

- $500 deductible

I would put the $5,004 into the replacement truck fund and self-insure.

The warranty company is betting that your covered repairs over the next 36 months will cost them less than $5,004 plus deductible income. Historically, that's usually a good bet for them.

For someone in your financial position and with a defined exit plan for the truck, I think self-insurance is the higher expected-value decision.

Sponsored

Now are you going to gamble on the SpaceX IPO

Now are you going to gamble on the SpaceX IPO