WhyNot21

Well-Known Member

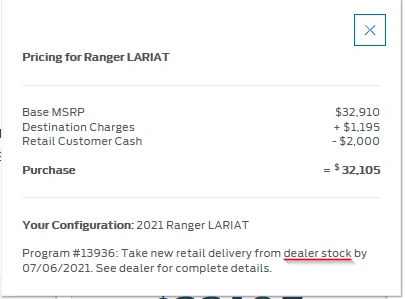

Obviously not.One question no one has addressed is... does an ordered vehicle qualify as "dealer stock"?

")

Edit: But it looks like it's at the dealer's discretion, just like the original question.

Sponsored

Obviously not.One question no one has addressed is... does an ordered vehicle qualify as "dealer stock"?

I am with you on this philosophy. I usually pay for my vehicles outright, and it is nice to have the freedom to sell quickly if needed. I have also done the other way. I bought my wife's CX-5 Carbon Edition, at 62 months 0% interests and there was no payment due for 3 months. I just could not turn down the free money. I financed my new 2021 Ranger with the dealer at the currently obscene rate of 5.9%, just to add, I am old enough to remember when that rate would have been a bargain. Dealer asked me to make 3 consecutive monthly payments for them to get the financing kickback. They cannot require it as there is no early payoff penalties allowed. But they gave me such a great deal on the truck (especially in todays pricing environment). I will pay off with the third payment, as I do not like to be a slave to a debt holder if I can help it. I know the math says to invest that money, but I prefer to live as debt free as possible. Currently only debt is the wife's car and my mortgage (2.49%).There is nothing wrong with being debt free. I took a zero interest loan and 6k off MSRP and paid off the truck in less than a year, did the same with my wife’s car. Dealers asked me to make six payments so their commission wouldn’t unwind.

To each their own, for me personally I like the feeling of actually owning a truck outright, don’t the like the concept of indebtedness.

Totally agree, the other part of the argument people who pay over time and ‘invest the difference’ is always left off. Sure they don’t pay a large amount up front, but they sure do on a monthly basis for years so their monthly cash flow for investing is diminished. The net difference factoring in dollar cost averaging in investments isn’t that big a deal, not to mention, stocks have been known (Feb 2020) to go down, leaving our investors without original principle and a big car debt. Again, no judgment here, to each their own, your results may vary.I am with you on this philosophy. I usually pay for my vehicles outright, and it is nice to have the freedom to sell quickly if needed. I have also done the other way. I bought my wife's CX-5 Carbon Edition, at 62 months 0% interests and there was no payment due for 3 months. I just could not turn down the free money. I financed my new 2021 Ranger with the dealer at the currently obscene rate of 5.9%, just to add, I am old enough to remember when that rate would have been a bargain. Dealer asked me to make 3 consecutive monthly payments for them to get the financing kickback. They cannot require it as there is no early payoff penalties allowed. But they gave me such a great deal on the truck (especially in todays pricing environment). I will pay off with the third payment, as I do not like to be a slave to a debt holder if I can help it. I know the math says to invest that money, but I prefer to live as debt free as possible. Currently only debt is the wife's car and my mortgage (2.49%).

That's when you buy, using capital not tied up in a vehicle.not to mention, stocks have been known (Feb 2020) to go down, leaving our investors without original principle and a big car debt.

I buy either way, just using funds not spent on car payments. We are both getting to the same place just using different roads,That's when you buy, using capital not tied up in a vehicle.

Mine were $4000 in April I think. Truck Month 1750 - Customer Cash - 1500 - Select Rebate - 750I bought the end of March and got $3000 manufacturers incentives that I believe were worded for cash sale. I thought it was weird they would give an incentive on a cash sale. I had a loan from my credit union so it counted as a cash sale as far as the dealer was concerned.

not exactly the same--I can pay the loan off at any time, but it's a lot harder to get low-interest cash back out of a truck you already own. regardless, people spend money on all kinds of things without any rational reason, and if some people want to get a lower return (effectively, spend money) because it makes them feel better to not have a loan, there's nothing wrong with that. it's just a shame when you see people who think there's something wrong with tools like loans, or that it always saves money to pay cash, rather than understanding that they may be paying a premium to feel better by using cash.I buy either way, just using funds not spent on car payments. We are both getting to the same place just using different roads,

I haven't had a 100% stock market AA for IIRC never. A paid off vehicle is a return that corresponds to the fixed income portion of your AA. It's the same with a mortgage. Too many people thought they were the arbitrage masters right before the GFC.not exactly the same--I can pay the loan off at any time, but it's a lot harder to get low-interest cash back out of a truck you already own. regardless, people spend money on all kinds of things without any rational reason, and if some people want to get a lower return (effectively, spend money) because it makes them feel better to not have a loan, there's nothing wrong with that. it's just a shame when you see people who think there's something wrong with tools like loans, or that it always saves money to pay cash, rather than understanding that they may be paying a premium to feel better by using cash.

Maybe I'm just overly risk averse, but taking out a loan to play the stock market doesn't sound like a very sound financial strategy.I bought my truck in April 2019. I could have paid cash instead of getting a loan...but the S&P500 return over the past 2 years has been around 40%. As long as you have the self-discipline to not blow the cash on hookers and booze, it makes no sense to not take a low-interest loan and put the cash to work.

I think it's just a few dealers that are trying to squeeze whatever they can out of a sale. I'll bet if people told them their walking if they had to use Ford to finance, they would change their tune pretty quick.When I purchased my XLT about two weeks ago, I got the $2,250 incentive. They asked if I wanted to finance, I said no and went in to pay with cashier's check no problem getting incentive.

Nothing, assuming sufficient reserves. Definitely don't play with money you don't have--using various tools to manage cashflow and liquidity is not the same thing as speculating on overleveraged margin. So what can you do if you lose your job and have a car loan? Well, if you have sufficient cash reserves (you must, you were going to pay cash, right?) you simply pay the monthly out of the reserves. In this case you're probably better off having a known monthly payment to budget for plus a pot of money instead of having no payment and no money because you spent all your cash on the car. That gives you time to figure out what to do, instead of needing to panic-sell the car to buy food or whatever.What happens when the economy tanks, I lose my job, my financed vehicle is upside down, and my stocks lost 40%?